Applying LEAP Options to Long Term Stock Moves

LEAPs are an attractive alternative to stock ownership. Not only do they have a better risk/reward profile, inexpensive LEAPs are easy to find and thus come with an inherent edge.

LEAP stands for Long-term Equity Anticipation Securities. As far as I’m concerned, LEAPs are just long-term options — longer term than the standard listed options. The only other thing special about them is that the exchanges consider them securities and allow brokerages to lend you up to 25% of their value. Not all brokerages honor this, however, and I wouldn’t recommend taking advantage even if yours will.

LEAPs are available with expirations one to three years out (currently January 2008 and January 2009) on hundreds of the most popular stocks and many indexes. Once a LEAP has only 9 months of life remaining, it converts into a standard listed option.

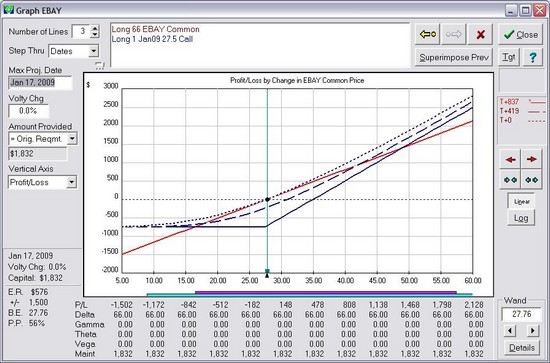

Let’s look at how an at-the-money call LEAP on EBAY would perform relative to an appropriate number of shares of the underlying shares of stock. The appropriate number of shares to use is determined by using the “delta” of the option. The delta of this option was 66, meaning that when the underlying moves one full point, the option theoretically moves 66 cents. Therefore a comparable position in the underlying would be 66 shares. That way if the underlying moves up one full point, we would gain $66 from the LEAP, or an equal $66 from the 66-share stock position.

In the illustration, the blue lines going highest to the right belong to the LEAP (The dashed line represents the performance of the LEAP in today’s time frame. The solid line represents the performance of the LEAP at expiration — 2+ years from now. The middle dashed line represents halfway between today and the expiration date.) The other solid red line represents the performance of the stock position.

That the two different positions have the same delta can be confirmed in the illustration. Note that the vertical wand marks the current price of the stock. At that point the LEAP’s current (T+0) (dashed) line and the stock’s (solid) line have identical slopes.

Risk/Reward

The LEAP has better characteristics to the upside, outperforming the stock by an ever greater margin the higher the stock price goes. To the downside, the LEAP is also better below a certain point. Although both a stock and a LEAP can go zero, in this example the shares of stock cost twice as much as the single LEAP (presuming you pay cash for the stock), thus the stock can lose more money.

In other words, the leap has better risk/reward characteristics because it is a call option. Just as with any call option, there is no limit to the upside, while the most you can lose is the investment.

Where the LEAP under-performs the stock is if the stock is still around its current price level two years from now. If that happens, the LEAP will have gradually decayed in value until it becomes nearly worthless. But who would expect the stock to be at the same price two years from now?

One caveat: If your stock is bought out, valuations in the LEAPs will collapse. Sure, your LEAPs may be helped by a jump in the stock price, but at the same time almost all of the time value will come out of them, and you may end up worse off than if you simply owned the shares. This shouldn’t be a worry, however, if your companies are unlikely takeover candidates (e.g. Cisco or Home Depot).

Len Yates is the President and founder of OptionVue Systems International and has earned worldwide recognition for his groundbreaking work in options analysis software. He has published numerous books and articles on options analysis and trading strategies, and is a primary contributor for the educational site DiscoverOptions.com.