Connors Research Traders Journal (Volume 35): The VIX Is Above Its 200-Day Moving Average. Now What?

I’ve been publishing VIX research since 1995. At the time the VIX was fairly new, and outside of Bloomberg, there were few mainstream vendors even offering data on it.

Moving ahead 24 years to today, the VIX is widely cited, has picked up the nickname “The Fear Index”, and most traders and investors follow it closely.

In spite of its nearly 3-decade existence, and it’s broad dissemination, it is still a bit mind-boggling to see so many articles that state the VIX has no predictive ability (therefore implying it’s useless!).

Today I’m going to share with you over 28 years of VIX data to show you that based on the data, VIX does have predictive ability. I’ll also show you why this information matters, especially in the current market environment.

Brief Background on VIX

Briefly stated, the VIX is the “implied” volatility of the S&P 500. It’s where market participants believe market volatility will be over the next 30 days. The VIX doesn’t look backward (historical volatility does), it looks forward as do the many other implied volatility indexes the CBOE offers (go to the CBOE.com website for a full list – while you’re there subscribe to their free newsletter because it’s an excellent resource for options and volatility traders).

Looking At the VIX On A Daily Basis

We recently asked two questions to further see how the VIX impacts daily movement in both itself and in the S&P 500 on a daily basis.

1. Does the behavior of volatility change when the VIX is above its 200-day moving average like it has been since early December?

2. Does the behavior of the S&P 500 change when the VIX is above its 200-day moving average?

The quick answer is yes to both. And here’s the hard data to support this.

We looked at VIX since its inception in 1990 through the end of 2018.

We asked…

1. How does the VIX behave each day it’s above its 200-day moving average versus when it’s below its 200-day average?

2. We also asked how the S&P 500 behaves each day when the VIX is above and below its 200-day moving average.

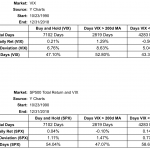

Here Are Test Results:

Four things stand out…

1. When the VIX is above its 200-day ma, it has risen the next day on average 1.29% vs dropping 0.50% when it’s been below its 200-day ma

2. As you would expect from #1, the S&P 500 has lost 0.10% per day when the VIX has been above its 200-day ma vs gaining 0.14% a day when it’s below. This is nearly a 1/4% difference in daily performance going back nearly 3 decades!

3. Look at the volatility (standard deviation) of the daily returns of SPX when the VIX is above its 200 ma vs when it’s below. It’s nearly double. Once the VIX goes above its 200-day ma, the volatility of the market dramatically increases.

4. On a directional basis you can see that since 1990, there has been a large difference in market direction depending on where the VIX stood compared to its 200-day ma. The market has risen the next day 58.62% of the time when the VIX has been below its 200-day versus only 47.07% of the time when its been above its 200-day ma.

How To Apply This Information

The reality is, at least looking back to 1990, one should have strategies in place to take advantage of the times the VIX is below its 200-day ma and separate strategies in place when the VIX is above its 200 ma.

The number of ways to do this is vast (I could write a book on this). For today though, the VIX has been above its 200-day moving average since early December, For long-only traders, it’s been treacherous since early December. For the short side traders, and long volatility traders, the past month and the first two days of January have been a bonanza.

The VIX will eventually move back under its 200-day moving average again and as it does, market behavior will likely change back again.

Wrap-Up

Going forward, it’s a solid idea to keep your eyes on the VIX relative to its 200-day ma. Nearly 3 decades of data is a large sample size and the current market behavior is consistent with the long-term results. For now, expect heightened daily volatility. And please be careful here because as you’ve seen over the past month, there are a lot of smart people out there, and none have been able to pick a bottom. It’s always wiser to wait until the statistical edges are in your favor!

Free Webinar – Swing Trading College 2019 and a Discussion on Current Market Conditions

The increased movement in stock prices has lead to greater opportunities. In order to take advantage of these opportunities, I will be conducting our next Swing Trading College (STC) beginning on January 16. Over 1000 traders have graduated our Swing Trading College and it remains our most popular training program.

If you’d like more information on STC, I’ll be conducting a 1-hour live webinar on Monday, January 7 and Thursday, January 10 at 1 pm ET. I’ll also be discussing current market conditions and sharing with you my outlook for the markets in 2019.

To attend the webinar, or to receive a recorded copy, please sign up here.

Sincerely,

Larry

Larry Connors

Connors Research, LLC.

P.S.

My new book Buy the Fear, Sell the Greed – 7 Behavioral Quant Strategies for Traders, is now available. Click here to order your copy today.

Receive The Connors Research Traders Journal Free To Your Inbox

CLICK HERE to sign up to receive new issues of the Connors Research Traders Journal newsletter directly via email up to 3 times a week!